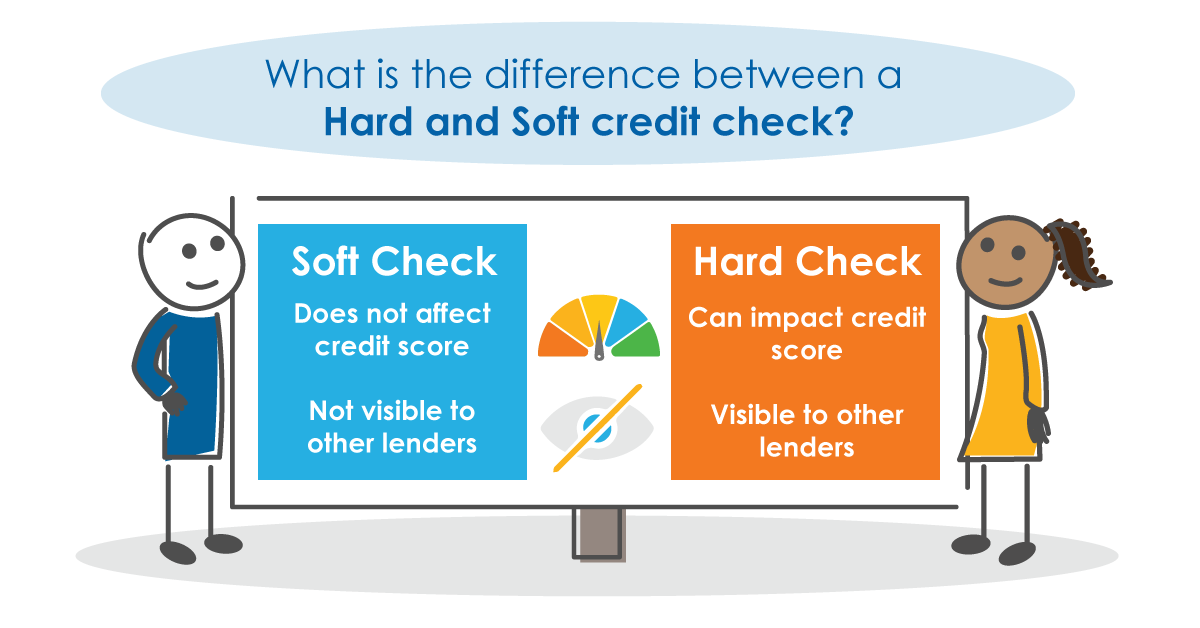

A soft credit check does not affect your credit score and is not normally visible to other lenders. A hard credit check leaves a visible search on your credit report and may affect your credit score.

Go Car Credit starts with a soft quotation search when an application meets our minimum criteria. We only complete a hard credit search later, after the finance agreement has been signed and the application is ready to proceed.

This guide explains how soft and hard credit checks work, what other lenders may see and when each search may be used during a car finance application.

What is a soft credit check?

A soft credit check, also called a soft search, allows a company to look at certain information from your credit report without recording a full credit application.

The search may appear when you look at your own credit report. However, it is not normally visible to other lenders and does not affect your credit score.

Experian explains that only you can see soft searches on your Experian report. It also says that soft searches do not affect your credit score or future credit applications.

A soft search may be used to:

- provide a quotation

- check whether you may meet initial lending criteria

- show your possible eligibility for a credit product

- confirm some of the details in an application

- complete an identity or anti-fraud check

- allow you to view your own credit report

Applying through a soft credit check car finance process means a hard search is not completed when you first apply to Go Car Credit.

Does a soft credit check affect your credit score?

No. A soft credit check does not affect your credit score.

You may see the search when checking your own credit report. Other lenders should not normally see it when they review a future credit application.

Equifax confirms that soft credit searches do not affect your credit score. It also explains that they may be used when a company wants to assess your possible eligibility for credit.

There is no credit-score penalty for having more than one soft search. However, a soft search result does not guarantee that a full credit application will be accepted.

What is a quotation search?

A quotation search is a soft credit search. It lets a lender look at some of the details on your credit report.

It does not leave a hard search mark on your credit report. It also does not affect your credit score. Other lenders will not normally see it.

The search may help a lender decide whether to look at your application in more detail. It does not mean that your application has been approved.

The lender may still need to check:

- who you are

- where you have lived

- your income

- your regular spending

- your current debts

- whether the repayments look affordable

- the car you want to finance

These details are part of how lenders use your credit information when they look at an application.

When does Go Car Credit complete a soft credit search?

Go Car Credit completes a quotation search after you apply and meet our minimum criteria.

This is a soft credit search. It does not affect your credit score. Other lenders will not normally see it.

The search helps us check the details in your application. It does not mean that your application has been approved.

We may still need to carry out more checks before making a decision. These checks form part of the car finance approval process.

Why might Go Car Credit complete another soft search?

Go Car Credit may complete another quotation search if you add a new address to your application.

For example, you may add an old address after the first search. We may then use another soft search to check for credit information linked to that address.

This extra search will not affect your credit score. Other lenders will not normally see it.

Can you have more than one soft credit check?

Yes. You can have more than one soft credit check. They do not affect your credit score.

A soft search may be used when you:

- use a credit eligibility checker

- compare credit products

- ask for a quote

- check your own credit report

- change details in an application

A car finance eligibility checker may show whether you meet the basic rules before you apply.

This does not mean that you have been approved. More checks may still be needed.

What is a hard credit check?

A hard credit check, also called a hard search, leaves a visible mark on your credit report.

Other lenders may be able to see this mark when they check your credit report in the future.

At Go Car Credit, lending checks are completed using soft quotation searches. The hard search is completed later to show that the finance agreement has been agreed and started.

Does a hard credit check affect your credit score?

A hard credit check may cause a temporary change to your credit score.

There is no fixed number of points that every person will lose. Credit reference agencies use different scoring systems, and the effect may depend on the other information in your credit history.

Several hard credit applications within a short period may have a greater effect. Some lenders may take recent searches into account because they could suggest that a person has applied for several forms of credit at once.

Experian says that each hard check may lower a credit score and that several hard checks over a short period may affect the outcome of later applications.

This does not mean that one hard search will stop you from obtaining credit. Each lender uses its own criteria and makes its own decision.

When does Go Car Credit complete a hard credit search?

Go Car Credit does not complete a hard credit search when you first apply.

A hard credit search is completed later, once the finance agreement has been signed and the application is ready to proceed.

This leaves a visible footprint on your credit report, which other lenders may be able to see.

The search is separate from the finance account itself. Once credit has been taken out, information about the account may also be reported to the credit reference agencies.

Does the Go Car Credit hard search mean finance has been paid?

Not by itself. A hard search records that a credit application search has taken place.

At Go Car Credit, the hard search is completed after the agreement has been signed and the application is ready to proceed. However, the search footprint and the credit-account record are two separate entries.

The account record may later show information such as:

- when the agreement started

- the current account balance

- the agreed monthly payment

- whether payments have been made on time

- whether the agreement is open, settled or in arrears

The account record forms part of the wider process of how car finance works after an agreement has been completed.

How long does a hard search stay on your credit report?

The time may vary between credit reference agencies.

Experian says most hard searches stay on its credit reports for 12 months.

TransUnion says searches stay on its reports for two years.

You can also read Equifax guidance on hard and soft credit searches.

A hard search is not the same as a credit account. Details about a credit agreement may stay on your report for a different length of time.

What is the difference between a credit search and a credit account?

A credit search records that an organisation accessed your credit report. A credit account records information about credit that you have taken out.

A hard-search entry may show:

- the organisation that completed the search

- the date of the search

- the type or purpose of the search

- the personal details used to find your report

A credit-account entry may show:

- the lender’s name

- when the account started

- the amount owed

- the account’s payment history

- whether the account is open or closed

- any missed payments or arrears

Understanding how to review your credit profile may make it easier to identify these different entries.

Hard and soft credit checks compared

| Credit-search question | Soft credit check | Hard credit check |

|---|---|---|

| Does it affect your credit score? | No | It may cause a temporary change |

| Can other lenders see it? | Not normally | Yes, while it remains on your report |

| Can you see it on your own report? | Yes | Yes |

| What is it normally used for? | Quotations, eligibility checks and initial assessments | Formal credit applications and final lending checks |

| Does it guarantee approval? | No | No |

| When does Go Car Credit use it? | After an application meets our minimum criteria and when further address checks are needed | After the agreement has been signed and the application is ready to proceed |

What information may a lender see during a credit check?

What a lender can see may depend on the type of search and the credit agency used.

Your credit report may show:

- your name

- your current and past addresses

- whether you are on the electoral roll

- credit cards, loans and finance agreements

- your payment history

- late or missed payments

- defaults

- County Court Judgments

- bankruptcy or other debt details

- past credit searches

The Information Commissioner’s Office explains what credit agencies may hold about you. It also names Experian, Equifax and TransUnion as the three main credit agencies in the UK.

A lender will not usually use your credit score on its own. It may also check your application, its own rules and whether the repayments look affordable.

This means there is no single credit score needed for car finance that works for every lender or every person.

Can you check your own credit report without affecting your score?

Yes. Checking your own credit report is a soft search.

It does not affect your credit score. Other lenders will not see it as a credit application.

The ICO says you can ask the credit agencies for a free copy of the information they hold about you.

You can get your credit report from:

Each agency may hold different details. This is because lenders do not always share data with all three agencies.

Checking more than one report may help you see more of your credit history.

What should you do if you do not recognise a credit search?

First, check the company name on your report.

The name may be different from the brand you know. It may show the lender’s legal name or the name of its wider group.

TransUnion says you should contact the company that made the search if you need more details.

If you still do not know the search:

- contact the company shown on your report

- ask why it checked your credit report

- check for other details you do not know

- tell the credit agency if you think the search is wrong

A search you do not know does not always mean fraud.

It is still a good idea to check it.

Is no credit check car finance available?

Lenders need enough details to check a credit application. They must also check whether the repayments look affordable.

Be careful with claims about car finance with no checks at all.

Some firms may mean that they start with a soft search. This is not the same as having no checks.

The term no credit check car finance may therefore mean that no hard search is used at the start.

Frequently asked questions about hard and soft credit checks

Will applying to Go Car Credit affect my credit score?

The quotation search completed at the start of our process does not affect your credit score.

A hard search is completed later, after the agreement has been signed and the application is ready to proceed. This hard search may affect your credit score and will leave a visible footprint on your credit report.

Does a soft credit search mean I have been accepted?

No. A soft credit search does not mean that you have been accepted for car finance.

It only helps us make an early check. We may still need to check your credit history, identity, income, spending and the car before we make a decision.

Can Go Car Credit complete more than one soft search?

Yes. Another quotation search may be completed if new address information is added during the application.

This may help us check for relevant credit information linked to that address. It remains a soft search and does not affect your credit score.

Can other lenders see a Go Car Credit quotation search?

No. A quotation search is a soft search and is not normally visible to other lenders.

You may still see it when checking your own credit report.

Can I have several soft credit checks?

Yes. Having several soft searches does not affect your credit score.

They may appear when you compare products, request quotations, use eligibility tools or check your own credit report.

Can several hard searches affect a car finance application?

Yes, they may. A lender may look at recent credit applications when it checks your credit history.

Several searches do not always mean that your application will be refused. Each lender uses its own rules.

Can I remove a hard search from my credit report?

You cannot normally remove an accurate hard search that resulted from an application you made.

If the search is wrong or you do not recognise it, contact the organisation named on your report. You may also ask the credit reference agency to investigate the entry.

Is a hard search the same as a credit agreement?

No. A hard search shows that a company checked your credit report.

At Go Car Credit, the hard search is completed after the agreement has been signed and is ready to proceed. The finance agreement may also show as a separate record on your credit report.

Is a hard credit search always completed for car finance?

A lender will normally complete a hard search before entering into a car finance agreement. The exact point at which it happens may differ between lenders.

Go Car Credit completes its hard search after the agreement has been signed and the application is ready to proceed.

Does Go Car Credit offer guaranteed approval after a soft search?

No. A soft search does not mean that your application has been approved.

We still need to check that you meet our rules and that the repayments look affordable. This is why guaranteed car finance does not mean that every applicant will be accepted.

Understand the search before applying for credit

A soft credit check may help you explore your options without affecting your credit score. A hard credit check leaves a visible footprint and is normally used during a formal credit application.

Go Car Credit starts with a soft quotation search when an application meets our minimum criteria. Further soft searches may be completed if new addresses are added during the application.

The hard search is only completed after the finance agreement has been signed and the application is ready to proceed.

Knowing which type of search will be completed may help you make a more informed choice before applying for bad credit car finance.