A Hire Purchase Agreement is a popular way to buy a car as it allows you to get the vehicle you want without having to lay out a large sum upfront. In fact, around 92% of car sales in the UK are completed using a finance arrangement.

At Go Car Credit, we specialise in helping those who have ‘bad credit’ secure a car finance agreement that suits them. That means even if you have black marks on your credit history, we may be able to help you fund your vehicle through hire purchase too.

To make sure you know everything you need to about hire purchase agreements, we’re going to look at the ins and outs of financing your next car using this method.

What is a Hire Purchase Agreement?

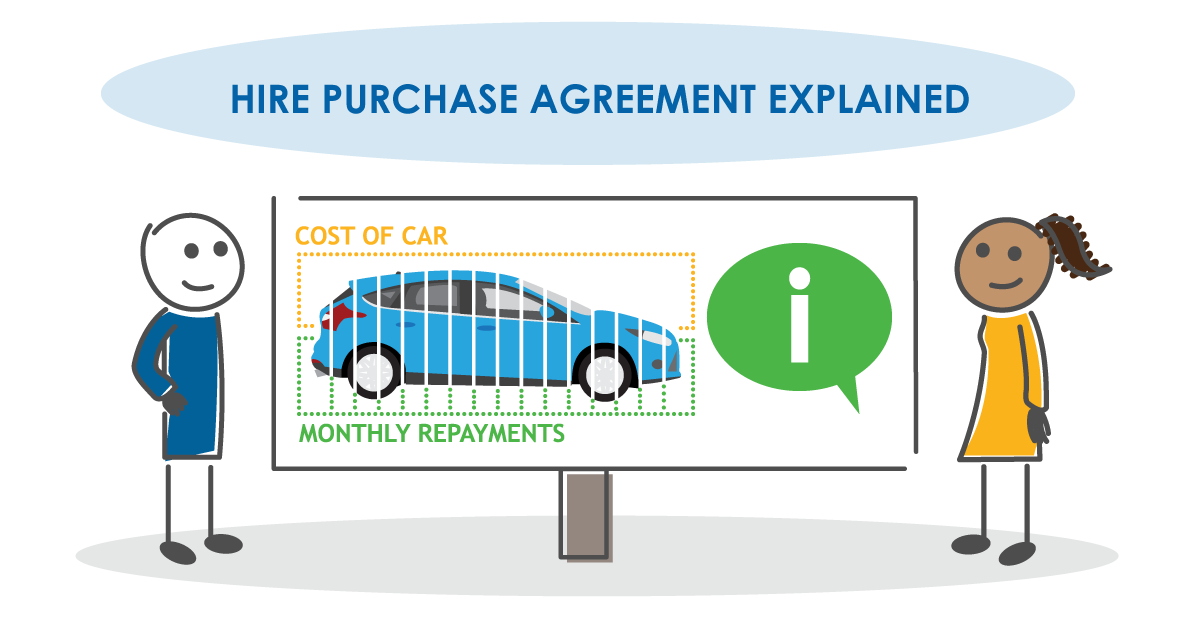

A Hire Purchase Agreement allows you to buy a car by making monthly payments, in place of paying the full cost upfront. Whilst you’re paying off your vehicle monthly, this is considered the ‘hire’ part, as the car is still owned by the finance company. Once you’ve made the last payment of the agreement, you’ll then have fully paid off the agreement and own the car.

It’s important to note that the monthly payments will be agreed between you and the finance provider beforehand and can vary depending on how expensive the vehicle is that you choose. Interest payments and additional fees are also added onto these payments.

What Details are Included in a Hire Purchase Agreement Document?

A hire purchase agreement is legally binding and so must clearly state the terms of the agreement.

At Go Car Credit, we like to keep things clear and simple, so here’s a breakdown of the key points included in the agreement:

- The specific vehicle being purchased on finance

- Amount financed

- The cost of each monthly instalment and the cost of the final price

- The dates on which the instalments will be paid

- Withdrawal period

- Additional fees and charges (such as interest)

Hire purchase agreement FAQs

The above list states some of the most important details that must be featured in the document, below are some of the most commonly asked questions regarding the agreement.

Will interest and APR be added?

On top of the base cost to pay for the car, you will also be shown how much you will pay in fees and interest. This extra amount is known as the annual percentage rate (APR).

For more guidance and a representative example, please visit our Hire Purchase Car Finance page.

When will I be the registered owner of the vehicle?

As soon as you get the keys to your new car, it will be yours to drive, and you will be the registered keeper. However, until you have paid off your monthly instalments, Go Car Credit will be the legal owner.

When do I receive the vehicle?

Many of our network of approved dealers offer same-day drive-away. So, once you’ve signed the paperwork, and have given your vehicle a test drive you’ll be able to take it home straight away.

Is car insurance included in the agreement?

Car insurance won’t be included as part of your hire purchase agreement and as every car in the UK is legally required to be insured, you must ensure that you get insurance just as you would if the vehicle was bought outright. When you take out a hire purchase agreement with us, you must take out comprehensive insurance on your car. This is to protect you against risks like theft, damage, or an accident.

Can You Get Out of a Hire Purchase Agreement?

There are different ways to get out of a hire purchase agreement, depending on how far into your repayment schedule you are.

- If you change your mind in the first 14 days after signing your agreement, you can contact us to cancel the contract. However, you will still be required to pay for your car.

- You can choose to repay the amount you owe early. At Go Car Credit, we don’t charge early repayment fees to our customers when they do this.

What Happens if the Vehicle is Stolen?

If your vehicle is stolen, the first thing you should do is call the police on 111, and they will give you a crime reference number. You can use this number to let your insurance provider know the situation, so they can begin your claim.

The next thing you should do is let the lender know, as the car is their asset. Once you’ve fully paid off the car and are the registered owner, you won’t be required to let the lender know. Insurance claims can take a few months, however, you must keep up your repayments during this period.

It’s possible your car may be recovered and returned to you. However, this may not happen, and you will need to use your insurance payout to settle the balance of your hire purchase agreement. It’s possible that this may not be enough to cover the total cost of your repayment, in which case we’ll offer support to help you cover this gap.

What Happens at the End of a Hire Purchase Agreement?

Congratulations! You’ve now repaid everything you owe. After paying a £10 purchase fee with your last instalment, the car is now yours to own. At Go Car Credit, we don’t hide sneaky costs or balloon payments into our plans either, so you won’t have anything else to pay.

Bad credit doesn’t have to keep you off the road. Check out our repayment calculator and let’s see what we can do to secure your next set of wheels.