A good credit score can change depending on the credit reference agency used. Experian, Equifax, and TransUnion are the most used credit reference agencies in the UK but they all differ in how they use credit scoring. Here we explore the difference between Experian and Equifax credit scores to help you understand what a good credit score can look like.

What is a good Experian credit score?

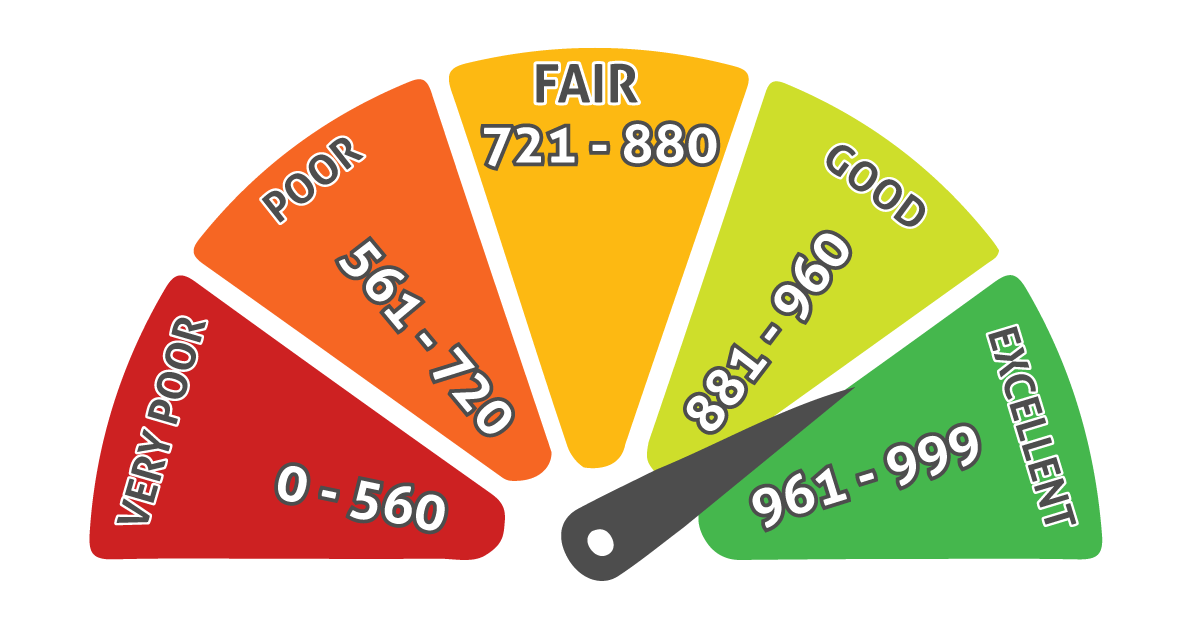

961-999 = Excellent

This is at the top end of the Experian scale, and most lenders would regard people in this category to be very low risk. This is because they would expect very few people with credit scores in this region to have problems making repayments.

881-960 = Good

People that have a score between 881 and 960 would most likely be viewed as low-risk by lenders. Lenders would expect few people in this category to be experiencing serious issues with repaying their credit.

721-880 = Fair

Lenders would expect people that have scores of between 721 and 880 to be a moderate risk. The expectation is that a small number of people in this category may experience severe problems with repaying their credit.

561-720 = Poor

Those with a credit score between 561 and 720 would be classed as high-risk by lenders – people in this category may have a history of not paying bills on time or may have simply not built up enough credit.

0-560 = Very Poor

These scores are at the lowest end of the table, and people that have a credit score of between 0-560 are likely to be classed as very high risk by lenders. Lenders may expect those falling into this category to have severe problems with repaying credit.

What is a good Equifax credit score?

Previously, the Equifax credit score scale ranged from 0 to 700 and was organised into five bands: very poor, poor, fair, good and excellent. However, Equifax revamped its credit scoring in 2021 to reframe its scoring categories and numbering.

The Equifax credit scoring guidelines are now as follows:

811 (and above) = Excellent

This score is at the top end of the Equifax scale, and most lenders would regard people in this category to be very low risk. People in this category have a positive history of credit that could have been built up by paying bills on time and not missing payments.

671-810= Very Good

People that have a score of between 671 and 810 would most likely be viewed as low-risk by lenders.

531-670 = Good

Having a score between 531 and 670 means you’d be a moderate risk for lenders.

439-530 = Fair

Those with a credit score of between 439 and 530 would be classed as high-risk by finance lenders.

0-438 = Poor

These scores are at the lowest end of the table, and people that have a credit score of between 0-438 are likely to be classed as very high risk by lenders. This is because lenders would expect those falling into this category to have severe problems with repaying debts.

What is a good TransUnion credit score?

TransUnion credit scores go up to 850 which use the VantageScore 3.0 as a way of scoring.

- 781-850 = Excellent

- 721-780 = Good

- 661-720 = Fair

- 601-660 = Poor

- 300-600 = Very poor

Do I have a bad or good credit score?

Lenders may only use your credit scores as a part of their decision-making process. Ultimately, they will assess your creditworthiness and affordability, which is a combination of how you have paid off previous credit commitments and your current ability to afford any new loans.

You may find you have a low credit score if you have defaulted on past repayments or have a CCJ which could be perceived as having a bad credit score.

Learn more about what credit score is needed for car finance as well as finding out how to repair credit before applying.

How to access your credit report

Your credit report will include varying degrees of detail depending on the level of access that you pay for.

You can get your credit score from any of the three credit reference agencies when you join a monthly monitoring service via a free trial.

Statutory credit report

A statutory credit report is a one-off snapshot of your credit report and credit history. It contains financial information about you, and lenders will use it to make a decision whenever you apply for credit.

We have plenty of informative guides on credit – from understanding your credit score and the role it plays in car finance to learning how to improve your credit score. Read our guides to credit here.

For more information about getting car finance if you have experienced bad credit in the past, check out our resources section, where we have information dedicated to these topics.